Saving tax legally is not about hiding income—it’s about smart planning. Every taxpayer in India has the right to reduce their tax burden by using government-approved deductions, exemptions, and investment options. In this 2026 guide, we will explain simple and effective ways to save tax legally.

1. Choose the Right Tax Regime

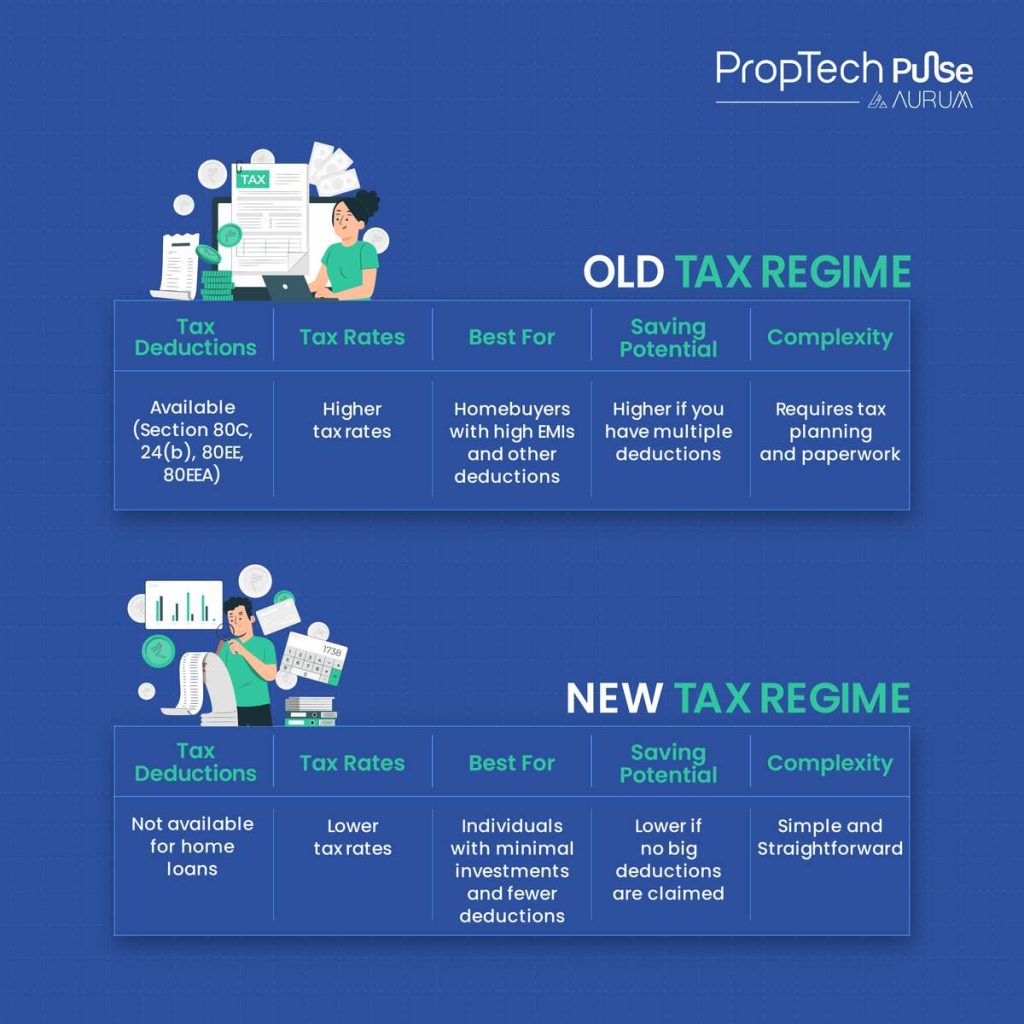

In India, you can choose between the Old Tax Regime and the New Tax Regime.

The Old Regime allows deductions and exemptions.

The New Regime offers lower tax rates but fewer deductions.

If you invest and claim deductions, the old regime may help you save more tax. Otherwise, the new regime might be better due to its simplicity.

2. Use Section 80C Smartly

Section 80C is one of the most popular ways to save tax. You can claim deductions up to ₹1.5 lakh per year through:

Public Provident Fund (PPF)

Employee Provident Fund (EPF)

Life Insurance Premium

Equity Linked Saving Scheme (ELSS)

National Savings Certificate (NSC)

Tuition fees for children

Investing in these options not only saves tax but also builds long-term wealth.

3. Claim Health Insurance (Section 80D)

Health insurance is essential today. Under Section 80D, you can claim deductions for premiums paid:

Up to ₹25,000 for self and family

Additional ₹25,000 for parents (₹50,000 if they are senior citizens)

This is a great way to protect your health and reduce tax at the same time.

4. Save Tax on Home Loan

If you have taken a home loan, you can claim:

Up to ₹2 lakh deduction on interest (Section 24)

Up to ₹1.5 lakh on principal repayment (Section 80C)

Buying a house not only gives you security but also significant tax benefits.

5. Claim HRA and Rent Benefits

If you live in a rented house, you can claim House Rent Allowance (HRA) to reduce taxable income. Even if you don’t receive HRA, you may still claim deduction under Section 80GG.

6. Invest in NPS (Extra Benefit)

The National Pension System (NPS) provides an additional deduction of ₹50,000 under Section 80CCD(1B), over and above 80C limits. It is a powerful tool for retirement planning and tax saving